The latest numbers appear less alarming when looking across a two-year time horizon, rather than solely comparing to 2021’s record-breaking tallies. By historical standards, funding totals are still pretty high. Early- and seed-stage dealmaking, for instance, is actually above 2020 levels.

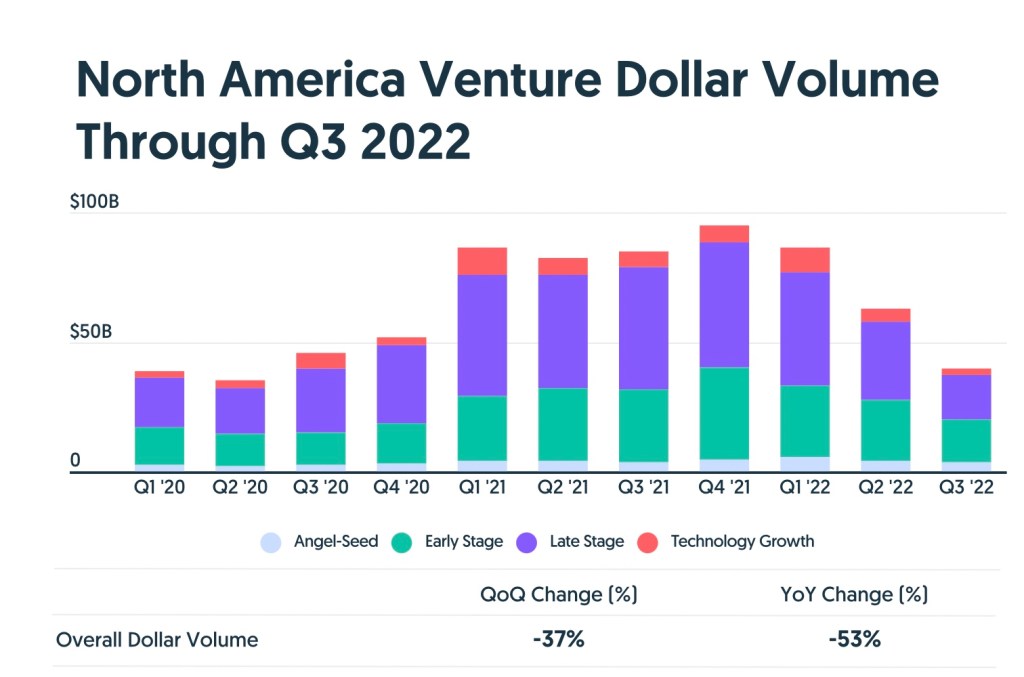

North American startup investment for the third quarter totaled less than half its year-ago levels, driven by an even steeper drop in late-stage financing.

It shows the pullback that commenced earlier this year has intensified in recent months, as tech valuations in public and private markets contract and the IPO window remains largely shuttered.

Overall, investors put $39.7 billion to work in seed- through growth-stage deals in Q3, down 53% year over year and down 37% from Q2. The year-over-year decline was most pronounced at late stage, which was down 63% in the just-ended quarter.

Late-stage and tech growth contract sharply

We’ll start with late stage, which saw the sharpest slowdown.

Altogether, late-stage venture and technology growth funding totaled $19.4 billion in Q3. That’s a drop of nearly two-thirds from the $53 billion invested in the year-ago quarter. Funding is also down about 45% from Q2.

Public markets may be driving much of the pullback in late-stage private markets. With tech and biotech shares down sharply on major exchanges, investors are rethinking valuations. Additionally, with few IPOs happening, pre-IPO rounds aren’t getting done either.

Even as late stage contracted, we did see some big rounds. The largest late-stage funding recipients for Q3 include digital manufacturing startup VulcanForms ($355 million Series C), small business policy provider Pie Insurance ($315 million Series D), and urban greenhouse company Gotham Greens ($310 million Series E).

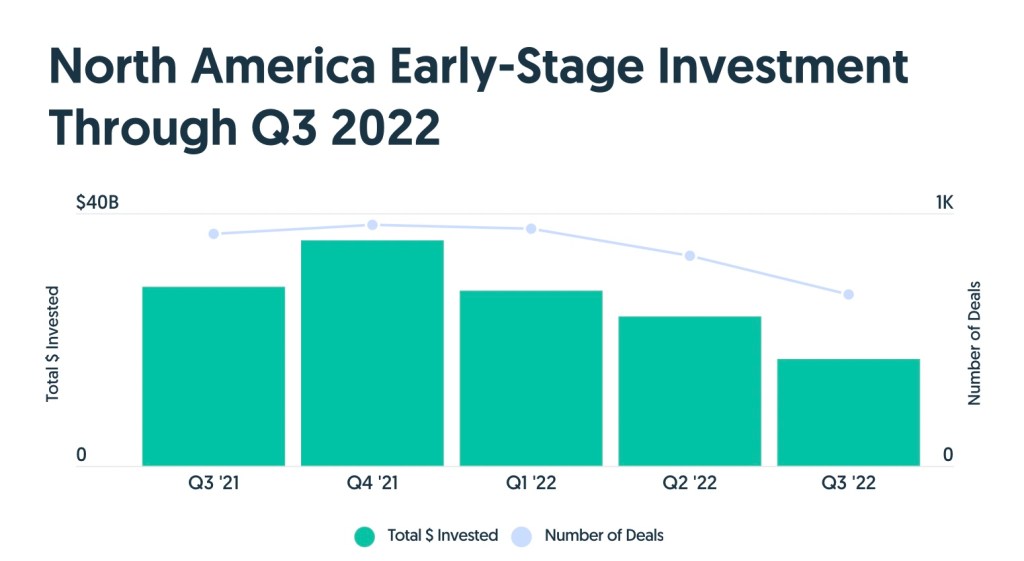

Early stage is down, but less so

Investors also tapped the brakes on early-stage dealmaking. For Q3, they put $17 billion into 879 known funding rounds. In dollar terms, that represents a 40% drop from the year-ago total and a 28% drop from Q2.

Early stage is showing a less dramatic decline than late stage in part because companies are further from exit. Apparently, there’s more confidence that market conditions will improve as these startups mature.

By far the largest early-stage deal of the quarter was a $1 billion Series A for TeraWatt Infrastructure, which provides charging stations for electric fleets. Next up was a $350 Series A for Areteia Therapeutics, a spinoff working on asthma treatments, followed by a $300 million Series B for Mysten Labs, a developer of Web3 infrastructure.

Seed stage’s comparatively strong showing indicates that investors are more confident about the long-term outlook than the short-term one. Also, while odds of failure are higher for newly minted startups, valuations are lower, which helps mitigate the risk.