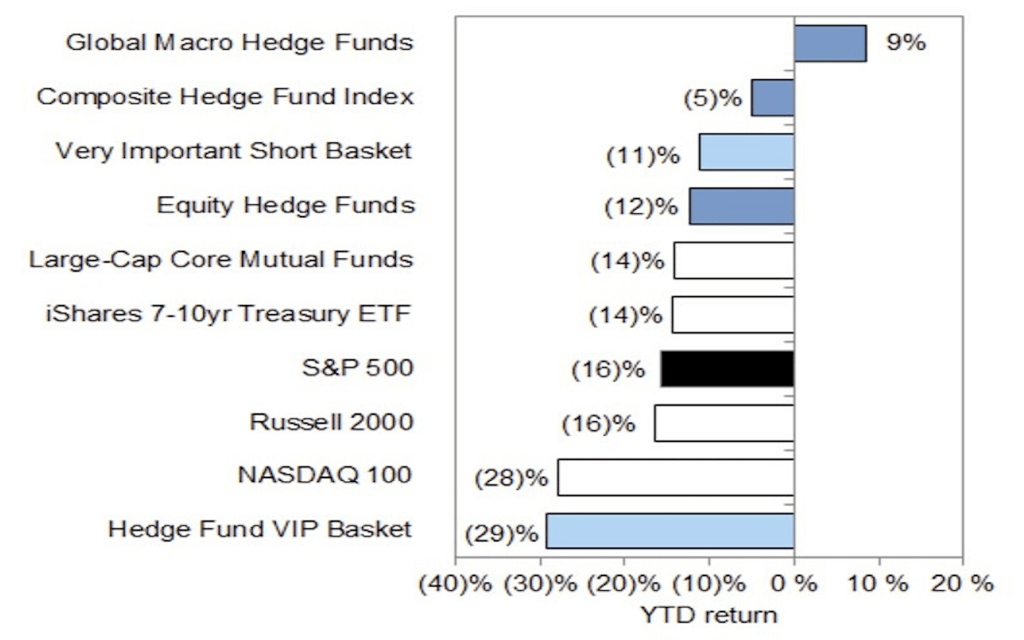

Hedge Funds have done better on average than the S&P 500 this year.

The average hedge fund has made a 1% return since the middle of the year, and is down 5% so far this year. And while that might not sound amazing, that’s still 11 percentage points better than the S&P 500’s 16% dip.

Hedge funds that trade based on global macro trends have done even better, chalking up a 9% gain this year: after all, they’ve had a whirlwind of opportunities ranging from geopolitical volatility to central bank rate hikes to inflationary concerns.

Hedge funds have turned their back on “momentum strategies” – that’s when you generally trade alongside the markets sustained price trend – so far in the final quarter 2022. After all, momentum-based strategies generally outperform during periods of market stress like in 2009, 2012, 2016, and 2020. And since hedge funds’ low net leverage hints that they have doubts about the markets’ movements right now, refusing to follow market price trends could make sense.

And while hedge funds usually go for more growth stocks, they’ve held more value stocks than usual over the past year. But because growth stocks did well during the third quarter, hedge funds picked up enough of them to bring the balance back toward the 20-year average.

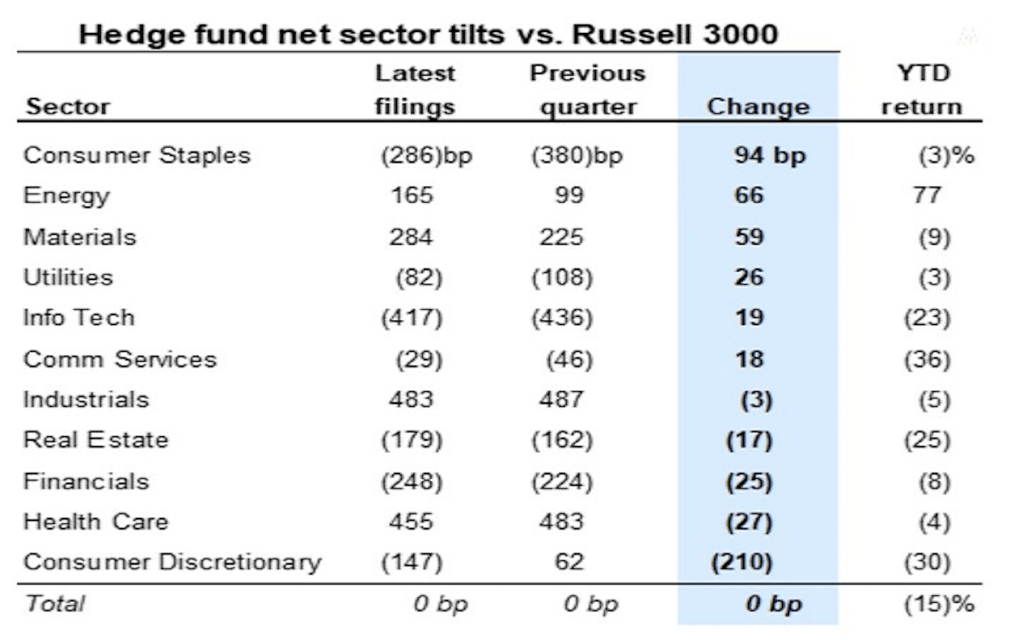

Hedge funds didn’t play around with their sector allocation much over the third quarter, but they did shift away from consumer discretionary stocks (that’s firms that make nice-to-haves) and toward consumer staples (that’s firms that make stuff folk need no matter what). They also added more energy and materials stocks to their roster. Information Technology stocks still make up the thickest proportion at 21%.

The main takeaway here is that hedge funds are allocating more capital to defensive sectors, based on their returns so far this year: that includes consumer staples, utilities, energy, materials, and industrials, which are all outperforming the Russell 3000 index’s 17% loss so far this year.