Stocks might be down this year, but $140-billion hedge fund Bridgewater thinks the bottom’s still to come. The world’s biggest hedge fund has compared today’s conditions to those of past inflation-driven bear markets, and it fears things have to get worse before they get better. Here’s why.

Bridgewater’s identified that bear markets tend to follow two stages:

1.Lower valuations. Rising interest rates reduce the present value of a firm’s future cash flows, because they increase the rate that’s used to discount them back to today. And since higher interest rates tend to cause all sorts of issues for the economy, they also hurt investors’ confidence, meaning they stay clear of stocks unless the risk premium seems high enough. So in order for stocks to look more attractive than holding cash, company valuations need to go lower. So far, that’s roughly what we’ve seen this year.

2. Lower earnings. This stage is less about valuations and market sentiment, and more about the actual economy and companies’ earnings. Rising interest rates lead to slower economic growth. However, the thing is, they impact different sectors of the economy with different lags, so not every sector will slow at the same time. So even if a leading sector like housing starts slowing down, companies’ earnings could still take a few months to follow suit. And if earnings then slow more than the market expects, as they generally do, stock prices will usually dip again. We arguably haven’t experienced that stage yet, but we might be getting a lot closer to it.

What needs to happen for stocks to rebound?

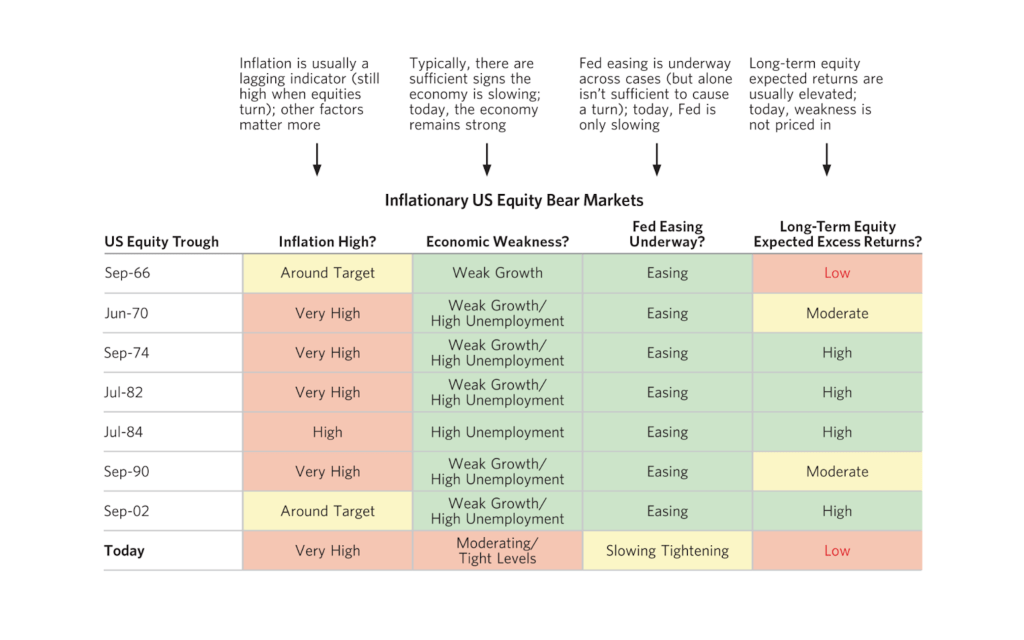

Bridgewater says three conditions must be in place for stocks to rebound in an inflation-driven recession. Firstly, the economy must be slowing sharply. Secondly, central banks need to ease monetary conditions – that’s cutting rates, not just slowing the pace of hikes. And finally, expected long-term returns from stocks must be high enough to incentivize investors to choose them over safer assets like bonds.

The table below shows (source: Bridgewater) that those conditions were set almost every time stocks rebounded in past inflationary bear markets:

Have stocks bottomed, then?

None of those conditions seem to be in place today. Here’s why.

The economy’s still too strong. Sure, some leading indicators – like the housing market and consumer confidence – have fallen off a cliff, and other metrics like the ISM Purchasing Managers Index (PMI) are slowing down too. But so far, key indicators like consumer spending and the labor market are still surprisingly strong.

The Federal Reserve’s (the Fed) far from cutting rates. The central bank might start slowing the pace of hikes down, or even pause the hikes in an extreme scenario. But inflation’s still way above target, and the labor market’s far too hot, for the Fed to actually pivot and start cutting.

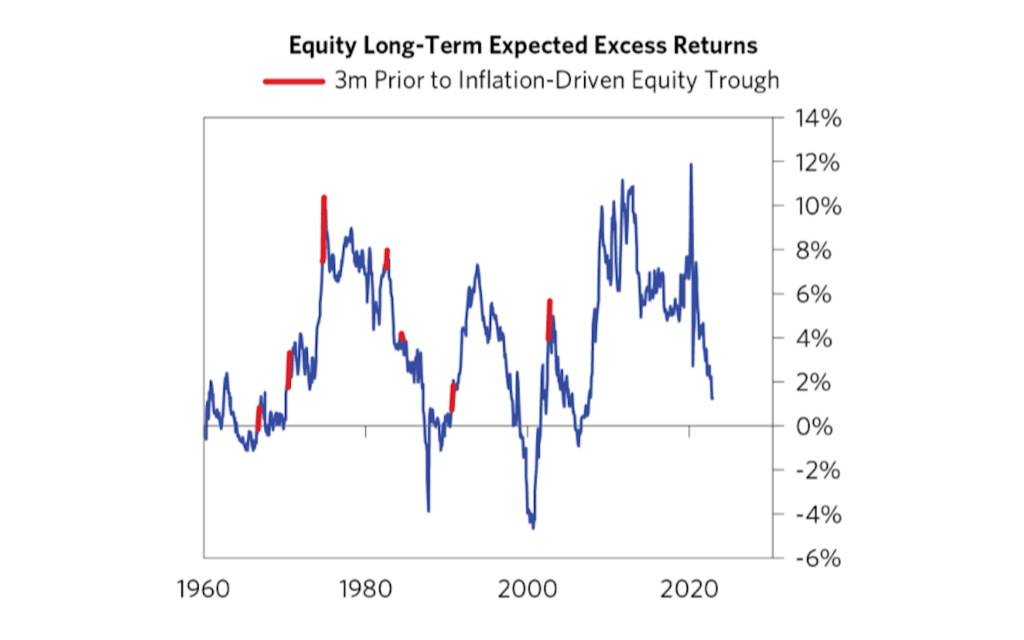

Investors are still wary of stocks. The S&P 500’s long-term expected returns look more attractive right now than at the beginning of the year, but they’re arguably still too low to draw investors back in. And given today’s yield levels, stocks are still relatively less attractive than bonds, so prices might have to go lower for investors to start buying stocks again.

If the Fed’s record interest rate hikes push the economy into a recession over the next few months, companies’ earnings might fall by more than the market currently expects – and stocks will likely feel the impact. That being said, sluggish economic growth could well push inflation in the right direction and allow the Fed to finally soften its aggressive monetary policy stance. At that point, Bridgewater’s rebound conditions might be in place.

If you think Bridgewater’s right, you might want to buy Treasury bonds: they should profit as the economy and inflation both get weaker. Gold might also do well, especially if inflation stays stickier than expected. But if you’re not sure what will happen next, your safest bet might be to buy a balanced portfolio of assets that generally perform well in different macroeconomic scenarios.