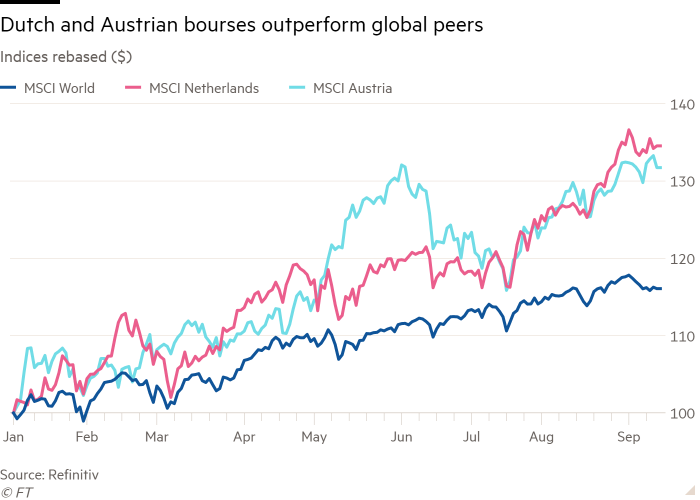

MSCI’s index of Dutch stocks has risen 34% in US dollar terms during 2021.

Two small European stock markets have produced some of the biggest gains in global equities this year, fuelled by companies benefiting from the chip shortage and a recovering oil price. MSCI’s index of Dutch stocks has risen 34 per cent in US dollar terms during 2021, while its equivalent Austrian index has gained 33 per cent, more than double the performance of the broader MSCI World benchmark. Both the Dutch and Austrian markets have shot ahead of the regional MSCI Europe index. The gains are partly fuelled by investors seeking exposure to Europe’s economic rebound from a short recession last year.

These index stories are very stock-specific.

Much of the strong performance of the Dutch stock market can be attributed to ASML, a maker of high-end lithographic machines for semiconductor manufacturers that constitutes 40 per cent of the MSCI Netherlands.

Investors expect burgeoning demand for ASML’s products as the US and the EU encourage more domestic chip production, striving to reduce manufacturers’ reliance on long semiconductor supply chains that have been disrupted by coronavirus. ASML’s shares have risen almost 90 per cent so far this year.

In Austria, oil and gas group OMV and electricity provider Verbund make up almost 45 per cent of MSCI’s stock index for the country. Shares in OMV have been on a tear, rising 54 per cent during 2021 after more than halving between January and October 2020 because of a slump in global oil prices that has since reversed. Shares in Verbund are up more than 30 per cent so far this year, contrasting with a drop of 1 per cent across the wider European utilities sector. Verbund says that almost all of the energy it produces comes from renewable sources, and is therefore popular with investors buying into the green energy trend.

Buy:

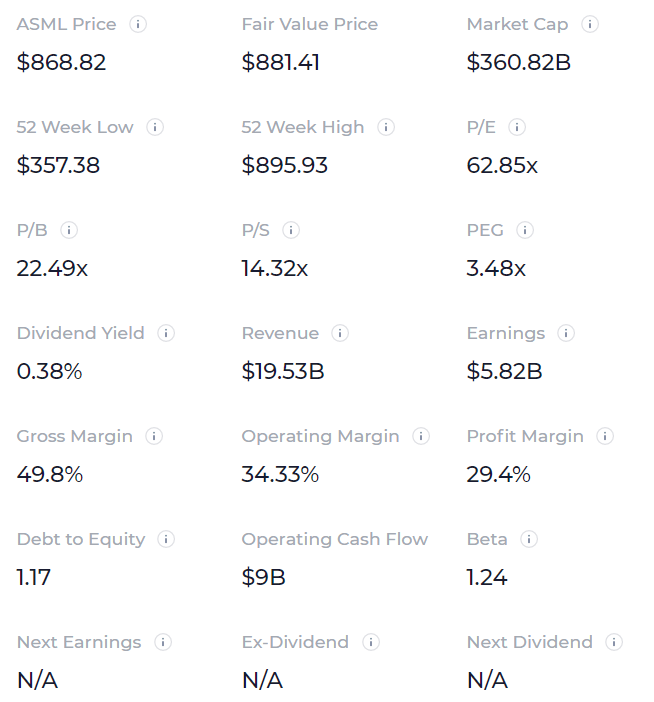

ASML ($868.82) is trading below its intrinsic value of $1,029.53, according to Benjamin Graham’s Formula from Chapter 11 of “The Intelligent Investor”.

ASML ($868.82) is undervalued by 1.43% relative to our estimate of its Fair Value price of $881.41 based on Discounted Cash Flow (DCF) modelling, but does not have a significant margin of safety.

ASML’s Earnings (EBIT) of $6.70B can safely cover interest payments on company debt ($5.44B)

ASML’s profit margin has increased (+5.8%) in the last year from (23.6%) to (29.4%)

ASML’s short-term assets ($19.43B) exceed its short-term liabilities ($10.30B)

ASML’s short-term assets ($19.43B) exceed its long-term liabilities ($8.39B)

ASML’s revenues are forecast to grow faster (13.38% per year) than the US Semiconductor Equipment & Materials industry average (11.89%)

ASML’s Return on Equity is forecast to be high in 3 years (54.76%); analysts are confident in the firm’s ability to efficiently generate return on equity.

ASML’s revenue has grown faster (23.98% per year) than the US Semiconductor Equipment & Materials industry average (20.84%)

ASML’s Return on Equity (35.6%) shows a company that is highly efficient at transforming shareholder equity into returns

However:

ASML is poor value based on its earnings relative to its share price (62.85x), compared to the US Semiconductor Equipment & Materials industry average (43.12x).